Just as spending a day under the summer sun without proper protection can leave you with a painful sunburn, an estate plan that does not carefully consider nontraditional parent child relationships can harm you or your loved ones. The Parent-Child Relationship

An effective estate plan will explore the parent-child relationship of everyone potentially involved. While inheritance rights may arise from the legal relationship between the parent and child, the scope, size and shape of any inheritance will depend on whether the deceased person completed any actions to create an estate plan. If no such plan exists or is invalid, then a child’s inheritance (or even a parent’s inheritance from a deceased child) will depend on the applicable laws prescribing a “one-size fits all” estate plan known as intestacy law. Intestacy laws determine who is entitled to inherit and how much the person in entitled to inherit. A few of the immediate questions to explore are:

When it comes to a child's legal ability to inherit from parents, adopted children and biological children are considered equal in the eyes of the law. However, situations involving stepchildren or presumed child can be more complicated. StepchildA stepchild is a child of one’s spouse or civil partner, but not one's own offspring, either biologically or through adoption. Unless the child is legally adopted, a stepchild has no legal right to expect an inheritance from a stepparent. The stepparent can however choose to provide for the stepchild in his or her estate plan. In that case, the stepchild would inherit from the stepparent in the same manner as any other beneficiary would inherit from the stepparent.  Presumed Child In some cases, a person may be considered a presumed child, which means a court recognizes the person as the child of the deceased, even if the person was not adopted. Legal recognition for presumed children is based on public policy that certain individuals should be treated as parents because of their relationship with a child and the role they assume in that child's life. The criteria for being a presumed parent can vary by jurisdiction, but they often include the following:

District of Columbia - Decedent's Child and Heir in EquityIn 2019, the DC Court of Appeals clarified, that the District of Columbia could recognize presumed children for intestacy purposes. The court held: if an individual seeks to establish that he is an intestate decedent's child and heir as a matter of equity, he must prove that the decedent objectively and subjectively stood in the shoes of his parent. In Re: Estate of Rosa North Ford, 200 A.3d 1207, 1215 (D.C. 2019). According to the Court, any person claiming to be the child of a deceased person and an heir as a matter of equity, “the putative child must prove that, as a minor, the decedent gave him a permanent home.” The Court further instructed that the probate court should consider the following questions:

Specific Gifts to Descendants or Do the Gifts Lapse? Parent and child relationship can be even more problematic when an estate plan makes specific gifts to friends and individuals who are not well known. These beneficiaries entitled to specific gifts are usually not the same as the residuary beneficiaries. When a beneficiary to specific gift predeceases the testator, the administrator of the estate plan must consider whether the gift will lapse or will the specific gift go onto the descendants of the predeceased beneficiary. This distinction will have significant consequences – if the gift lapses, then the gift will remain part of the estate and will be distributed to the residuary beneficiaries. If the gift goes onto the descendants of the predeceased beneficiary, then the residuary beneficiaries will not receive that potion of the estate constituting the gift. Therefore, the administrator of the estate plan must inquire into whether the beneficiary had children, biological, adopted or even presumed children in order to determine whether the gift can still be made. In the absence of perfect knowledge then the default rule should be that such gifts will lapse. ConclusionThe relationship between a parent and child can take many forms. It is therefore important that you discuss with your estate planning and financial advisors the need to have an estate plan that clearly identifies your intended beneficiaries and the legal relationship of those beneficiaries to you. Your discussion should also examine relationships with any individuals who may not be immediate or obvious family members. With a well thought-out, comprehensive estate plan, you can rest assured that your wishes regarding inheritance will be clear and properly documented so they can be legally enforced.

Green Book for 2024 (March 9, 2023) Green Book for 2024 (March 9, 2023) On March 9, 2023, the Biden administration offered budgetary proposals that could, if enacted, affect estate planning, particularly for high-income taxpayers, the administration of post-mortem trusts and decedent’s estates and the tax rules for trusts. These proposals are found in the Administration’s Green Book, which is an annual exercise explaining the administration’s budget for the next fiscal year. This discussion of the proposals affecting estate planning will be divided int a series of three articles, and this first article will address the proposals that target

The second and third articles will address the address the administration of post-mortem trusts and decedent’s estates and then the proposed changes to the tax rules governing trusts. Targeting High-Income Taxpayers’ Retirement Account Retirement Security vs. Wealth Transfer ToolBecause of the special tax treatment afforded retirement accounts, some high-income taxpayers use these accounts - not for retirement security – but as wealth transfer tools.  An individual is in the high-income category if their modified adjusted gross income is over $450,000 if married filing jointly, over $425,000 if head-of-household, or over $400,000 in other cases. In 2021, eighty-seven percent (87%) of taxpayers, sixty-years-old or older, had some type of retirement savings. These retirement accounts are consistent with the law’s purpose that retirement accounts such as IRAs, 401Ks and Roth IRAs serve to provide retirement security. However, as of 2022, the Joint Committee on Taxation estimates

The wealth transfer occurs when the taxpayer dies. The taxpayer’s heirs will inherit the accumulated assets, which grew tax free, without having to pay any income taxes being owed if the heirs follow the rules. (While not subject to income taxes, these inherited assets will still be included in the calculation of estate taxes.) Special Distribution Rules for Large Account Balances ($10 Million or More) To curb the excessive accumulation, a high-income taxpayer with an aggregate vested account balance in a Roth retirement account exceeding $10 million would be required to distribute a minimum of 50 percent of the amount exceeding $10 million. If the high-income taxpayer balance exceeds $20 million, then the taxpayer would be subject to minimum distribution amount (“floor”). This floor amount would either be set by

Elimination of Backdoor Roth IRAA backdoor Roth conversion is a strategy used by high-income earners who are prohibited from contributing to a Roth IRA because their income is above certain limits. Instead of contributing directly to a Roth, these high-income taxpayers contribute to a traditional IRA (which has no income limits), and then convert it to a Roth IRA. Under the proposal backdoor Roth conversion would still be permitted for taxpayers with income above the Roth IRA contribution limit, but below the high-income earner limit. Final ThoughtsWhile these are just proposals, if they became law the proposals as currently drafted would affect only the "fortunate few." Nevertheless, these proposals could become a trend that ultimately will touch ordinary people like us, our loved ones and our futures.

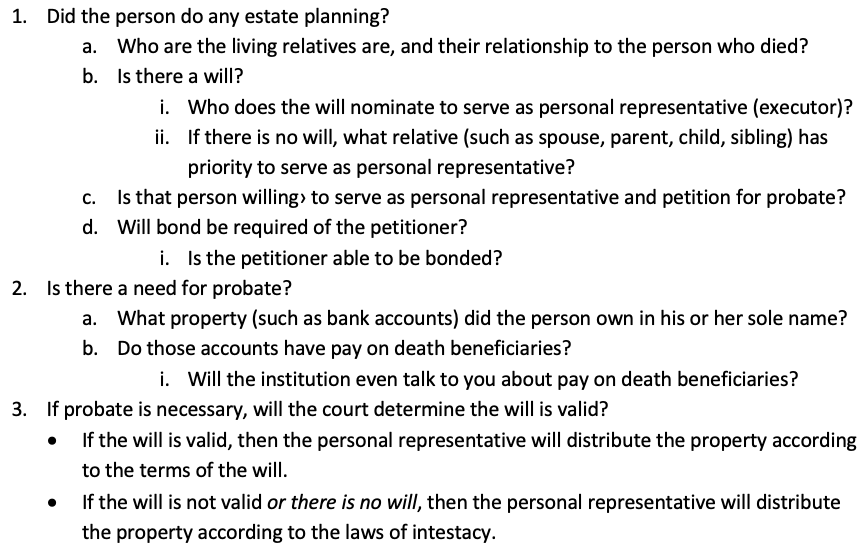

When a person dies, what happens next will depend on various factors. If the deceased person did not engage in trust-based estate planning, which our clients do, then probate will likely be required. Probate is a formal legal process of proving that a will is valid (if the person had a will) and appointing someone (executor, now known as the “personal representative”) to carry out legal obligations of paying creditors, paying taxes and supervising the distribution of the deceased person’s property. As discussed below paying taxes, paying creditors and distributing property can be done without involving the courts. Nevertheless, for people who do not engage in trust-based estate planning, probate will be required. Probate AnalysisThis analysis will help determine whether a probate case needs to be opened.  Probate ConceptsWhile probate rules can vary between D.C., Maryland and Virginia, below we examine some of the concepts relevant to probate anywhere. Deadlines Deadlines must be met. If the appointed personal representative fails to meet the deadlines, then the court may penalize the personal representative or even remove him or her as personal representative. Supervised or Unsupervised ProbateThe number of deadlines will depend on whether the court will supervise the proceeding. While most proceedings in D.C. are unsupervised, proceedings in Maryland and Virginia are supervised, which means the personal representative must file inventories and regular accountings Interested Persons The law dictates who is entitled to know about a petition for probate. The personal representative must identify for the court these “interested persons,” who must be informed of the petition for probate and then those interested persons, who must be informed of any filings with the court such as an inventory or accountings. If the person has a will, these interested persons will initially include the people named in the will (legatees) and people who otherwise would inherit if there were no will (heirs at law). This latter group, heirs at law, must be given the opportunity to contest the will. Once the will is admitted to probate then these heirs at law are no longer considered “interested persons.” When dealing with interested persons, even if there is bad blood, the personal representative has a legal duty to keep an interested person informed and to provide them with the information they are legally entitled to. Collecting and Securing the PropertyThe personal representative must locate and secure the deceased person’s money and property and create an inventory of all items. Tax IDsThe personal representative will likely need to obtain from the Internal Revenue Service a tax identification number for the estate and open an estate checking account for depositing estate funds and paying creditors and taxes. Notifying CreditorsThe personal representative must notify known creditors and attempt to find unknown creditors. Notice to unknown creditors is accomplished through publication. Generally, at the direction of the probate court, the personal representative must mail the notice to known creditors and pay for (or otherwise cause) a notice to creditors to be published in specific publications for the requisite period of time. This notice allows creditors, both known and unknown, to make claims against the estate for any debt owed by the deceased person. The personal representative must then determine the validity and priority of all creditor claims received and pay those claims as appropriate. Claim PeriodIf the personal representative follows the correct steps regarding the notice to creditors, then any debts not brought during the claim period may be extinguished once the claim period ends. With respect to untimely claims, the estate will be relieved of any obligation to pay such claims. Cutting off these claims creates legal certainty, so that the personal representative can ultimately close the estate and make the distributions of the deceased person’s property without worrying about future claims. Accountings  The personal representatives must maintain accounting records as proof of monies coming into and going out of the estate. Depending on the circumstances, the accounting records may need to be filed with the court, and interested parties may need to sign releases at certain intervals. Filing and Paying TaxesA personal representative must file the deceased person’s final tax returns (1040) for the period up to the date of death. The 1040 and equivalent state returns are due on the same day as if the deceased person were filing. The personal representative will then be required to file a fiduciary return (1041) for the remaining period until the estate is closed. If the deceased person was even moderately wealthy, the personal representative may have to file an estate tax return (706) and the estate returns for D.C. or Maryland (Virginia has no estate tax). These state returns flow from the information provided in the federal estate tax return. We Are Here to Help Avoid Probate Most of what needs to be done when someone dies can be done outside of court. Therefore, probate is an unnecessary burden which should be avoided. By focusing on trust-based estate planning, we help our clients avoid probate and stay out of court. If this sounds good to you then we can work with you to create an estate plan to take care of you and your loved ones with without going to court. If you would like to learn more about using a trust-based estate plan and what is involved, please give us a call.

|

Archives

December 2023

|

RSS Feed

RSS Feed

Services |

Company |

|